Quarter-point hike and healthy jobs report anticipated,ECB and Norway may also raise rates while Brazil stays on hold

Federal Reserve policymakers are about to extend their year-long campaign of raising interest rates to beat back still-stubborn inflation, even as risks to the US economy build.

The Federal Open Market Committee is expected to boost the benchmark lending rate target by another quarter percentage point on Wednesday, marking the 10th consecutive increase going back to March of last year. While officials’ efforts have helped to reduce price pressures in the US economy, inflation remains well above their goal.

At the same time, first-quarter growth figures this past week pointed to an economy that’s downshifting. The monthly jobs report on Friday will give a sense of how labor demand — a key support for the economy — is holding up.

US Employment Holding Up, Yet Hiring Pace Is Cooling

Source: Bureau of Labor Statistics, Bloomberg

The projected 180,000 increase in April payrolls is seen as healthy, although it would mark the third straight month of decelerating employment growth. The still-firm labor market has been instrumental in extending an economic expansion that’s increasingly feeling the pinch from tighter Fed policy.

Other data on the schedule include March job openings and April surveys of purchasing managers in manufacturing and services.

What Bloomberg Economics Says:

“Signs point to the FOMC raising rates by 25 basis points to 5.25% in the May 3 decision — despite ongoing turmoil in the banking system — and signaling that this will be the last hike for a while. The next phase of the tightening cycle will be to hold rates at that elevated level, while watching to see if inflation trends down.”

—Anna Wong, Stuart Paul, Eliza Winger and Jonathan Church, economists.

Elsewhere, rate increases in the euro zone and Norway and a pause in Brazil will be among other key monetary decisions due around the world.

Central Bank Rate Decisions This Week

Europe, Middle East, Africa

The region faces an eventful week, albeit a shorter one in many countries following a long holiday weekend.

The ECB takes center stage on Thursday with a rate decision in the wake of the Fed the previous evening. Investors and economists anticipate a quarter-point hike, dialing down the pace of tightening as the central bank’s earlier moves impact the economy with a lag and lingering financial-stability worries dictate caution.

What to Watch

Shortened week with crucial data in countdown to ECB meeting

Source: Bloomberg

Critical to the decision will be the ECB’s latest bank-lending survey, due on Tuesday, and inflation data published the same day.

The consumer-price figures are anticipated by economists to show conflicting signals: the headline measure could accelerate for the first time in half a year, while an underlying index stripping out volatile items such as energy may show slowing.

It’s that latter gauge that ECB officials are watching — and if the report were to show so-called core inflation unexpectedly quickening, a bigger rate move could yet transpire.

Euro-Zone Inflation Numbers Will Be Crucial for ECB

Source: Eurostat, Bloomberg Economics, Bloomberg surveys of economists

Other monetary policy decisions are also due from across the region:

- Danish policy makers normally follow any ECB rate move with a similar one of their own. Any hike is likely to transpire in the hours after the outcome in Frankfurt on Thursday.

- Earlier that day, Norway’s central bank may raise borrowing costs by a quarter point, keeping up pressure on inflation just as the economy proves more resilient than expected.

- The Czech central bank on Wednesday is expected to leave rates unchanged despite increasingly hawkish rhetoric from its board members.

It’s a quieter week in the UK, where officials will enter a blackout period before their decision on May 11. Among data due there are shop prices from the British Retail Consortium, Nationwide house prices, and the Bank of England’s mortgage approval and consumer-credit data.

Figures on Wednesday will probably show that fourth-quarter economic growth in Kenya slowed to 4% from 4.7% in the prior three months. That’s as unfavorable weather conditions, higher input costs, foreign-currency shortages, rising interest rates and government spending cuts curtailed output growth.

Turkish inflation is expected to remain high in data due Wednesday but price gains are anticipated to cool, with the Treasury Minister saying they’ll dip below 50%.

On Friday, Turkey’s trade balance may take another hit from a surge in energy and gold imports. Data for the country are being closely watched ahead of close-run elections on May 14.

Asia

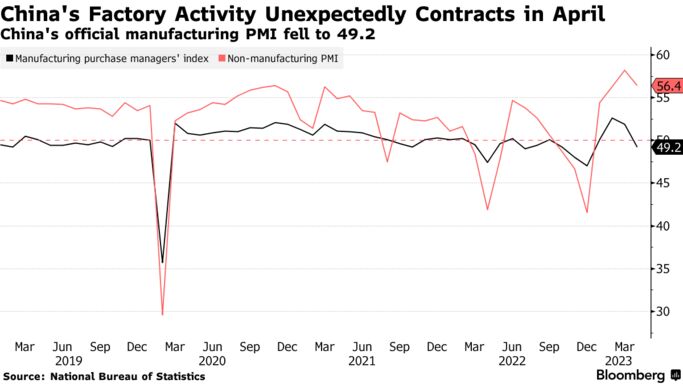

China’s latest PMI figures on Sunday showed an unexpected contraction in manufacturing activity in April, a sign the economic recovery remains patchy and may be struggling to sustain momentum.

That discouraging sign for the global economy from China is likely to be reinforced by South Korean trade figures out Monday that are forecast to show a gloomy outlook.

Inflation figures Tuesday should hint at whether the Bank of Korea’s decision to keep rates on hold is supported by cooling price growth. Regional PMIs the same day will fill out the picture for Asia’s current economic momentum.

Finance ministers and central bank governors are set to gather for the annual Asian Development Bank meeting in South Korea, with climate financing measures among the matters under discussion. Senior officials from both Japan and South Korea are expected to attend.

The Reserve Bank of Australia is expected to keep rates unchanged again as inflationary pressure Down Under continues to edge down from elevated levels.

Malaysia’s central bank is also seen standing pat on Wednesday. Indonesia, Thailand and Taiwan are all due to release price data during the week.

Latin America

The week kicks off with the April consumer price report for Peru’s capital, Lima, which likely slowed for a third month from 8.4% in March. Central bank chief Julio Velarde sees inflation hitting 3% by year-end.

Brazil Central Bank Can Hold Key Rate Unchanged for a Long Time

Policymakers seen keeping key rate at 13.75% for sixth meeting on May 3

Sources: Banco Central do Brasil; Bloomberg.

The bottom line of this week’s Brazilian central bank rate decision is a given — the key rate will be kept unchanged at 13.75% for a sixth straight meeting.

Any drama will come from the post-decision communique: Brazil watchers will be on the lookout for shifts to a standing warning that the bank won’t hesitate to lift rates to counter resurgent inflation.

In Colombia, publication of the central bank’s monetary policy report and minutes of its recent meeting may take a back seat to the April 26 ouster of finance chief Jose Antonio Ocampo by President Gustavo Petro, and subsequent tumble by the nation’s assets.

Disinflation in Latin America’s Big 5 Economies?

CPI is falling in Brazil, Chile, Mexico, Peru – Colombia may join them this week

Sources: National statistics agencies, central banks; Bloomberg.

Note: Peru, Colombia April 2023 data = economist estimates.

The week may, however, end on a propitious note. Data out of Colombia on Friday may show inflation slowed for the first time in 11 months from March’s 13.34%, perhaps even below 13%. With that, inflation in all five of Latin America’s big targeting economies would be falling simultaneously once again for the first time since April 2020.